1st Quarter 2024 Quarterly Compass Economic Update

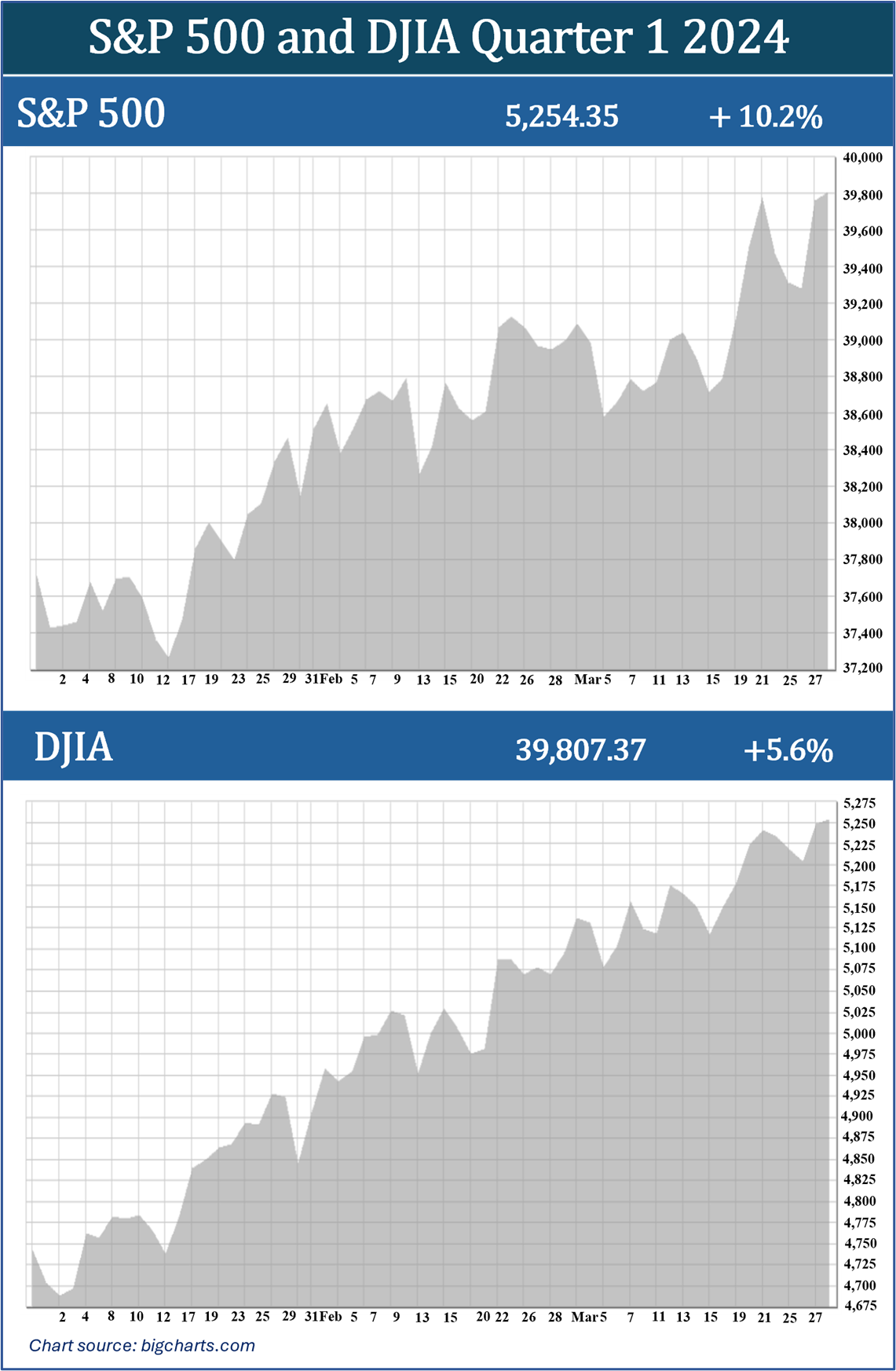

The first quarter of 2024 continued to reward investors who stayed the course and enjoyed strong returns in 2023 as the momentum of 2023’s year-end rally took another step forward. Both equity and bond markets performed well after the Federal Reserve confirmed that disinflationary trends were consistent and satisfactory enough for them to finally consider monetary easing beginning this year. The S&P 500 experienced its best first quarter since pre-pandemic in 2019. All three major indexes had strong finishes, and both the S&P 500 and the Dow Jones Industrial Average (DJIA) closed at record levels for the first quarter.

For the quarter, the S&P 500 returned over 10% and closed the quarter at 5,254. The Dow Jones Industrial Average finished the quarter at 39,807, adding over 5%. (www.investopedia.com; 4/1/2024)

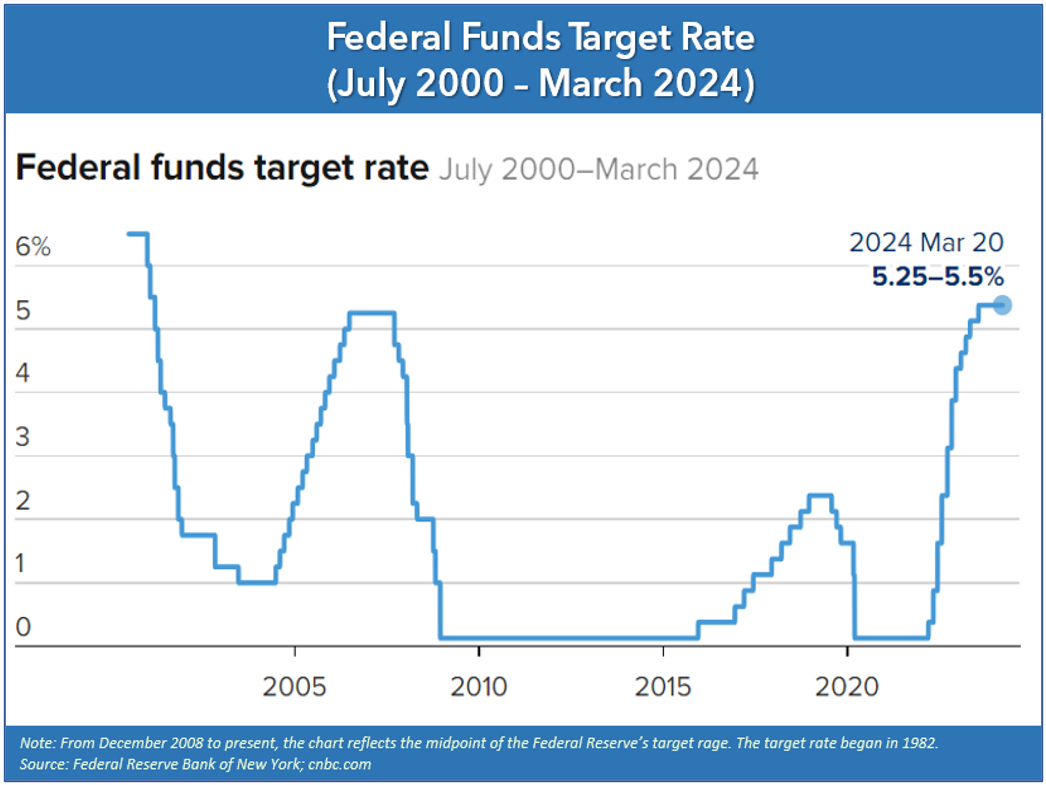

The resiliency of the U.S. economy continues to be impressive. Still facing the dragging feet of inflation and a healthy workforce, the Federal Reserve has affirmed that rate cuts are anticipated this year. However, as of the quarter’s end we did not see the Fed reduce interest rates. During their March meeting, the Federal Open Market Committee (FOMC) maintained the federal funds rate of 5.25 – 5.5% but signaled that rate cuts were still on the horizon. Equity markets responded favorably to the optimistic news.

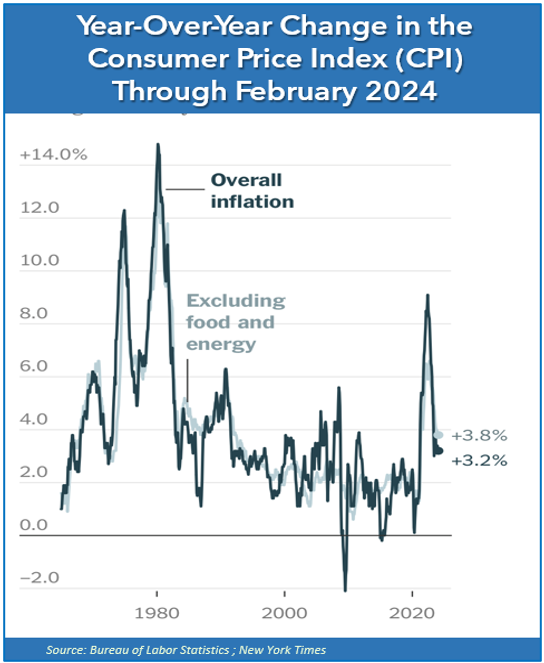

Inflation is still a major concern for investors and the Fed closely monitors the Consumer Price Index (CPI), which is a broad measure of goods and services costs. The CPI rose 0.4% in February and 3.2% from a year ago. The core CPI (CPI less food and energy) rose 0.4% for the month and was up 3.8% for the year. Energy costs increased 2.3%, which helped boost the inflation number. Gasoline, specifically, rose 3.6% in February, recouping January’s -3.2% adjustment. Shelter increased 0.4% on a year over year basis. These two components accounted for over 60% of the monthly increase in the CPI. Data from trips to the grocery stores and restaurants were stagnant, as food costs remained the same on the month. (Source: /www.bls.gov/news.release)

Shelter costs remain high. Shelter prices were up 5.7% in February. According to a weekly national survey of large lenders by Bankrate, the average mortgage interest rate was 7.07% on a 30-year loan as of March 20, 2024. Despite the high rates, existing home sales still rose 9.5% from January 2024 to February 2024 according to the National Association of Realtors.

(Sources: bankrate.com, 3/24/24)

March employment statistics, which are considered a strong measure of health in the U.S. economy, were stronger than expected, coming in at 3.8%. This number indicates that the U.S. economy is still strong. Investors are torn between wanting to see a strong economy to support earnings growth, but also wanting a weaker jobs market to give the Fed a signal to start reducing interest rates.

Overall, the first quarter of 2024 brought strong equity returns and bolstered investor confidence, however, we feel investors should be careful of becoming overoptimistic or complacent. We abide by our mantra of, “proceed with caution.” Now is a good time to review your investments and confirm they are still congruent with your time horizon, risk tolerance, and goals. As your financial professionals, we are committed to keeping you apprised of any changes and activity that could directly affect your unique situation.

Inflation & Interest Rates

Interest rates have not changed since July 2023, when the Fed raised rates by 25 basis points. The March 19-20, 2024, Federal Reserve meeting marked the fifth consecutive time in a row that rates were held steady at a range of 5.25-5.5%. The stock market’s immediate reaction was positive, with the S&P 500 gaining 0.3%, and the Dow Jones Industrial Average (DJIA) advancing nearly 0.4% that Wednesday afternoon after the Fed’s announcement.

The Fed statement released shortly after their March meeting concluded noted that, “Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.”

While the inflation rate is well below the peak levels of 9.1% in 2022, it is still not at the desired level of 2% that the Fed’s would like to see. During the Fed’s March meeting, the median 2025 and 2026 rate views were raised by three tenths of one percent to 2.9% and 3.1%, respectively, and the longer-run rate was lifted by one tenth of a percentage point to 2.6%. This means the Fed believes that their tighter policy could last longer than anticipated to get back down to their 2% target rate.

Despite slightly higher inflationary data, the Fed remained confident that inflation is still heading toward their 2% target rate. “I think they haven’t really changed the overall story, which is that of inflation moving down gradually on a sometimes-bumpy road toward 2%,” Chair Jerome Powell stated during a press conference immediately after the March Fed meeting. He continued, “We’re not going to overreact to these two months of data, nor are we going to ignore them.” (Source: cnbc.com, 3/20/24)

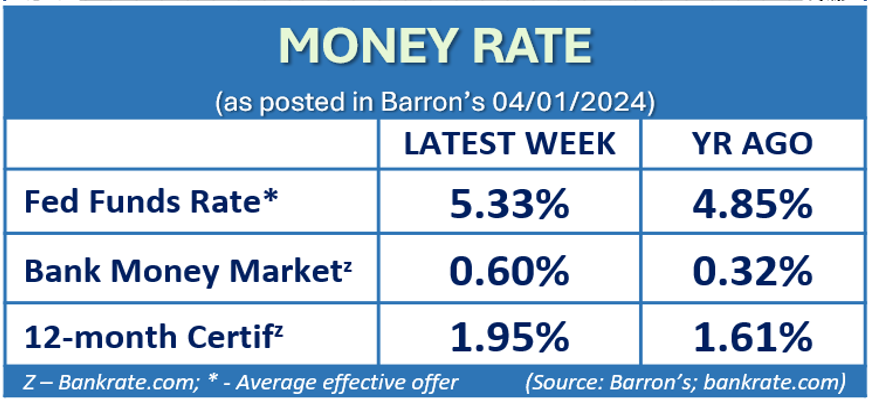

As of the quarter’s end, the Fed is still forecasting three rates cuts in 2024, despite the possibility that inflation may stay elevated for longer than anticipated. These pending rate cuts are highly anticipated as consumers have been coping with the highest rate range level in more than 23 years. While still lower than the all-time high of 20% in 1980, any rate cuts will be welcomed by consumers. (Source: tradingeconomics.com)

The Fed is committed to their goal of a 2% inflation rate and optimal employment levels and so they continue to keep a close eye on these and other key indicators. Their mandate is to carefully watch the economy and assess incoming data to make appropriate decisions on if and when to lower interest rates. According to their notes, until the Fed has “greater confidence that inflation is moving sustainably toward 2 percent,” they do not anticipate reducing the target range. (Source: federalreserve.gov, 3/20/2024 Press Release)

Interest rates and inflation are integral to investors and their financial planning, so we will continue to keep a watchful eye on any movements and stay apprised of key economic indicators.

The Bond Market and Treasury Yields

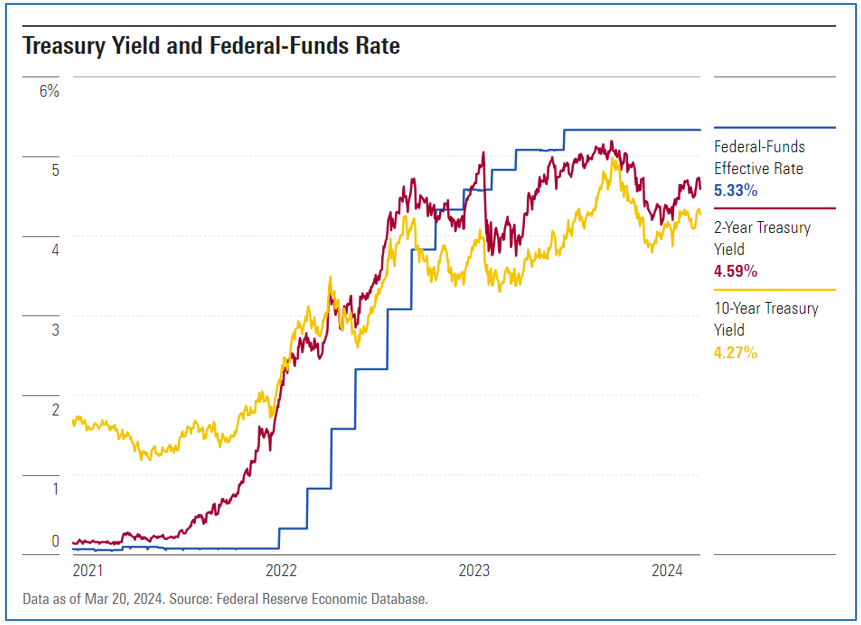

Treasury yields rose with news of stagnant interest rates cuts, continuing the long-standing inverted yield curve. This means that short-term bonds are yielding more than longer-term bonds.

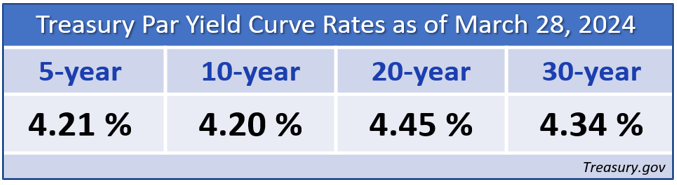

The quarter ended with the benchmark 30-year yield at 4.34% and the 20-year yield settled at 4.45%. As of the end of the first quarter, this inverted yield curve has remained longer than the previous record of a 624-day inversion in 1978. While many analysts consider an inverted yield curve as a precursor to a recession, we have yet to see an economic downturn, leaving optimism for the Fed’s prized soft landing. (Sources: Deutsche Bank; www.morningstar.com)

We will continue to closely monitor how the Fed’s movements are affecting bond yields. With the Fed anticipating interest rate cuts in 2024, this may narrow the opportunity to get lower-risk, higher yielding bonds. For anyone who is interested in exploring adding more bonds as part of a diversified portfolio, please contact us. As your wealth manager, we want to help you make the best decision for your portfolio. Please remember, while diversification in your portfolio can help you pursue your goals, it does not ensure a profit or guarantee against loss.

Investor’s Outlook

Although the year has started on a strong note, investors are always best served by preparing for volatility. Interest rate movements have been a major market influencer and how much, if, and when, are the three questions surrounding the Fed’s anticipated rate cuts this year. The Fed has indicated that this interest rates cycle has probably peaked. “We believe that our policy rate is likely at its peak for this tightening cycle and that if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year,” Powell said in March. He added that, “The general sense of the committee is that it will be appropriate to slow the pace of run-off fairly soon, consistent with the plans we’ve previously issued.” While the Fed is still looking forward to rate cuts in 2024 and beyond, the timing remains uncertain.

Currently, the U.S. economy continues to show signs of strength and resilience. Could we see that soft landing the Feds have been discussing the last few years for the United States? The Fed’s goal is to give us a soft landing and avoid a major recession.

While we may avoid a major recession, we believe volatility will remain due to several factors, including continued inflationary pressures, political uncertainty in the U.S., and continued global conflict. Geopolitical risks, deficit spending and problems in commercial real estate are also factors that could cause serious economic problems.

There are six remaining Fed meetings in 2024. If they delay cutting interest rates again, or possibly reducing the number of predicted cuts in 2024, this could adversely affect a market that many analysts feel is already priced for the three currently anticipated rate cuts. Any deviation from this strategy could shake investor confidence. With many unknowns ahead, it is always possible to see a market correction in the near future.

Most economists predict that, should a market correction (a decline of 10% or greater in the price of a security, asset, or a financial market) happen, it will be a modest one. According to the New York Fed, there is an over 58% chance that a U.S. recession (a significant, widespread, and prolonged downturn in economic activity) will happen within the next 12 months. (Source: barrons.com; 3/20/24)

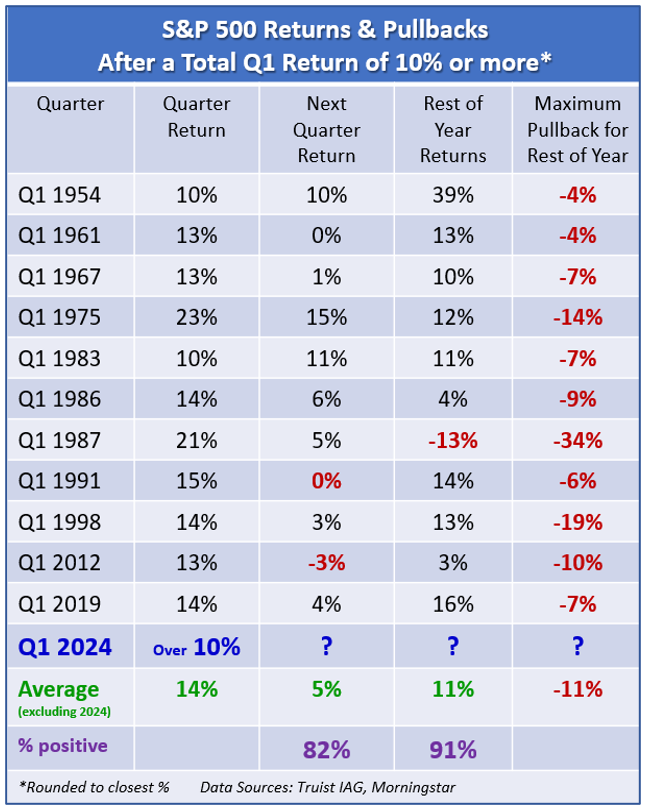

As the chart shows, since 1954, after a first quarter of more than 10% returns in the S&P 500, the second quarter was higher nine out of eleven times. All those years included pullbacks (a temporary retreat of no more than 5-10% in the price of a stock) during the year, however, ten out of those eleven years ended with positive returns, with an average of 11% (coincidentally the average pullback was also 11%). Please remember as with all data, past performance does not indicate or guarantee future results.

While the Fed projects rate cuts in 2024 and beyond, recent history has shown us, anything can happen in a very short amount of time. A re-acceleration of inflation or unsatisfactory data could deter the Fed from beginning rate cuts. Fed officials will be keeping a close eye on key indicators such as housing, labor markets, and core goods that will help them when determining monetary policy.

An area to keep an eye on in the coming months is housing costs. Despite higher interest rates, home values continue to be high. A correction is possible, but inventory is still low, and lending standards have been revamped following the housing crisis in 2008 during the Great Recession. This should help dissuade a major housing market crash. Housing economists believe that while housing prices may cool down, much to the enjoyment of buyers, we will not see a housing market crash.

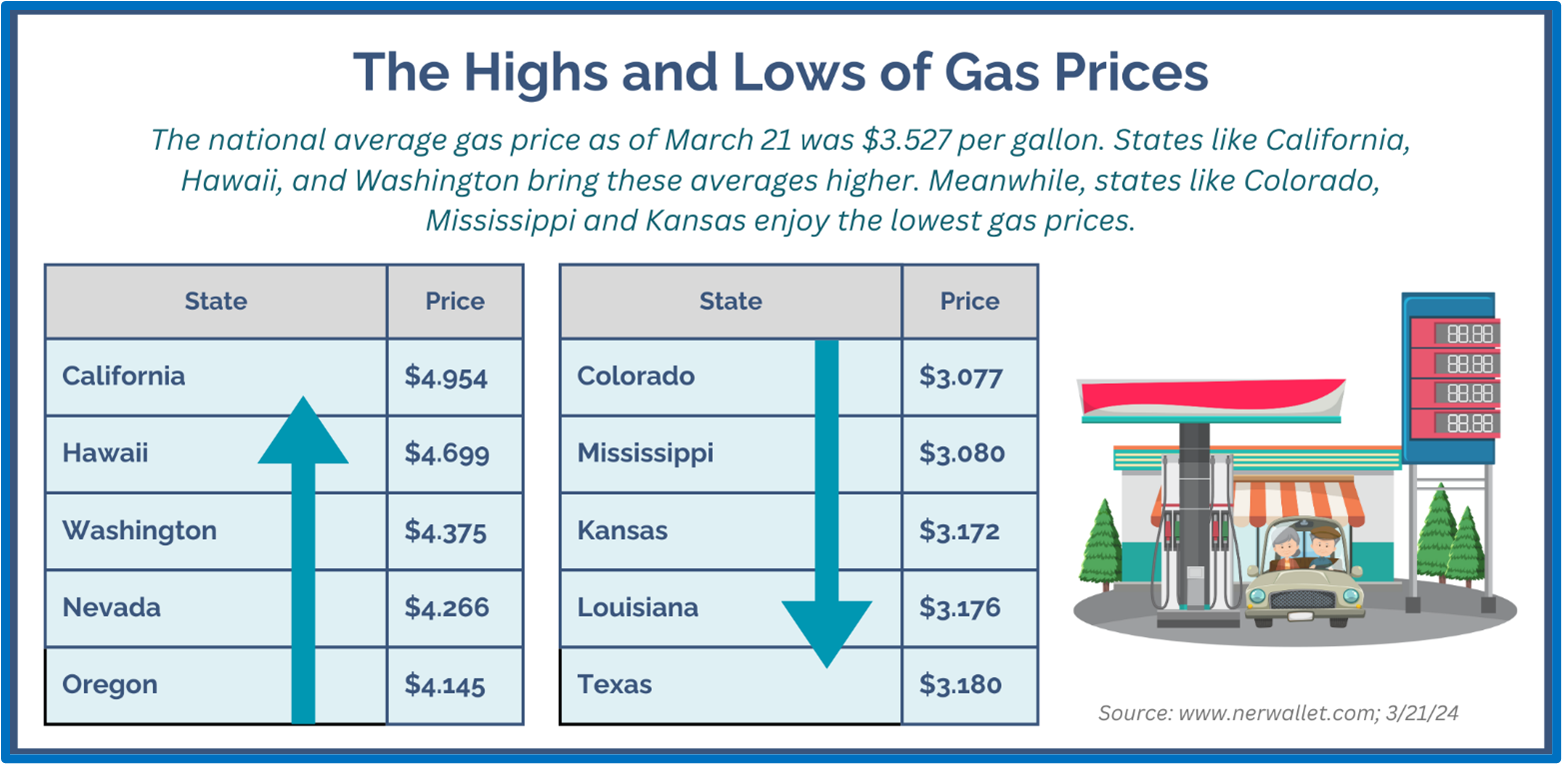

Although not in the core Consumer Price Index, seasonal gas prices can be a key player in inflation rate movement. According to AAA, since the beginning of the year, average gas prices have increased .44 cents as of March 21. Year-over-year data shows that gas prices on average are .09 cents higher. The good news is that gas prices are down about 30% from June 2022 when the highest average gas prices was over $5.00.

While economic and inflation trends typically affect equity markets more than election results, this year includes a presidential race that will keep everyone on their toes. There are also key races for the Senate and House of Representatives and election results could impact government policy and tax law, leaving much up in the air. We can be sure that the media will be hyper-focused on the upcoming election, however investors still need to remain focused on key factors such as economic growth, inflation movement, and interest rate changes when determining the best path for their investment decisions.

As mentioned earlier, as of the quarter’s end, equity markets were still experiencing a rally, however investors need to be prepared in case there is a potentially overdue pullback. 2023 and the first quarter of 2024 rewarded long-term investors and we stand by our belief that investing should be measured based on long-term results. We believe that volatility could still be prevalent and that investors should be cautionary when making any financial decisions. As always, a long-term strategy needs to be a benchmark for smart investors.

This is a time to stay vigilant and stay focused on your personal goals. Proactive preparation and providing you with a solid financial strategy that considers your risk tolerance, time horizon, and potential tax implications is our goal. We will continue to keep an eye on inflations rates, economic growth data, and monetary policy moves.

As always, before making any change to your financial situation, please contact us. We can help you assess your options and make sure your plan is still in alignment with your goals.

We want to exceed your expectations. We take pride in offering service that includes:

- A proactive, individually tailored approach to our client’s financial goals and needs.

- Consistent and meaningful communication throughout the year.

- A schedule of regular client meetings.

- Continuing education for our team members on issues that may affect our clients.

- Proactive planning to navigate the changing environment.

We always recommend discussing any changes, concerns, or ideas that you may have with us prior to making any financial decisions so we can help you determine your best strategy.

Please remember that as a valued client, we are accessible to you. Feel free to contact us with any concerns or questions you may have.

We appreciate the trust and confidence you place in our firm.

team@stablerwm.com | (425) 646-6327

Securities and financial planning services provided through LPL Financial, a Registered Investment Advisor. Member FINRA/SIPC.

Note: The views stated in this letter are not necessarily the opinion of broker/dealer, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice. This material contains forward-looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

The S&P 500 is an unmanaged index of 500 widely held stocks that is general considered representative of the U.S. Stock market. The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. There is no guarantee that a diversified portfolio will enhance overall returns out outperform a non-diversified portfolio. Diversification does not protect against market risk.

Sources: www.cnbc.com; www.federalreserve.com; www.tradingeconomics.com; www.bankrate.com; www.forbes.com; www.nerdwallet.com; Investopedia.com; www.morningstar.com; www.bigcharts.com

Category

Stay Informed

Join our mailing list to receive monthly newsletters with information that impacts your financial decisions.

Certified Financial Planner

In Business 35+ Years