3rd Quarter 2022 Economic Update

Investors understand that markets go up and also

go down. After being treated to better than

average returns for over a decade, 2022 has been

a year that has tested even the most seasoned of

investors. This year, investors have experienced frequent bouts of market-moving news, combined with reports of slowing economic growth, elevated

inflation, and weakening fiscal and monetary stimulus. In response, by the end of the third

quarter, the S&P 500 index tumbled nearly 25%

from its record high, and bonds have lost more than 14% since January. Investors have seen huge market volatility in response to many reports

including those on monthly inflation, jobs numbers and every utterance of Federal Reserve officials. With that type of backdrop, it can be easy for investors to get caught up in the here and now. Having said that, the most successful investors still acknowledge that investing success can be most consistently achieved with a long-term perspective.

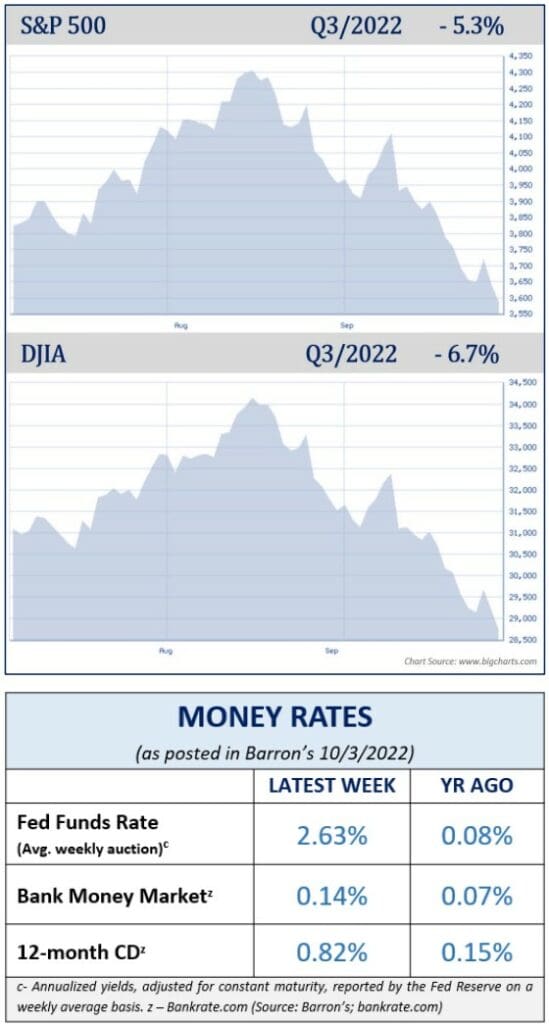

The third quarter of 2022 was a very rough one for

equities. September’s quick drop left the S&P 500

down 5.3% for the quarter. This marked a 52-week low, and September was logged as the worst performance for the S&P 500 since March 2020.

The Dow Jones Industrial Average (DJIA) also set a

52-week low, closing down 6.7% for the quarter.

This marked the third consecutive quarter decline,

bringing it down 21% to date for 2022. Similar to

the S&P 500, the DJIA experienced its worst month in September since the pandemic-driven lows in March 2020.

After a long hibernation, with a few peeks outside,

it looks as if the bear has officially come back to the equity markets.

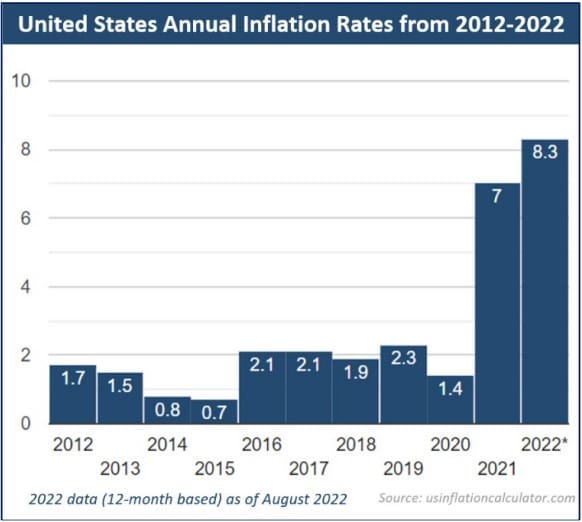

The annual inflation rate for the United States was 8.3% for the 12-months ending August 2022. Americans continued to feel the pinch as fuel prices and grocery receipts remained markedly higher.

During the quarter, first-time unemployment claims hit a 4-month low, which is both good news and bad news. The good news is more Americans have jobs, the bad news is the Fed, which takes unemployment rates into consideration when making adjustment, is likely to continue their aggressive tactics against inflation. Jefferies economist Thomas Simons wrote, “The labor market remains very tight, and the claims data do not show any signs that slack is emerging. If anything, the recent claims data suggest that the labor market is tightening up even more.” (Source: barrons.com, 9/29/22)

The Fed also looks at the impact of shelter costs when deciding policy moves. Housing prices still remain high in many areas of the country, even with the significant increase in mortgage rates and elevated rental costs.

“I think that shelter inflation is going to remain high for some time. We’re looking for it to come down, but it’s not exactly clear when that will happen. It may take some time. Hope for the best, plan for the worst,” Powell said during the September FOMC meeting. (Source: cnbc.com, 9/21/22)

Chief Economic Christopher Rupkey at FWDBONDS in New York, stated, “The Fed won’t be slowing the pace of their rate hikes yet with 75 basis points in November and 50 basis points more in December a virtual certainty.” Rupkey continued, “The Fed is going to go until something breaks, but so far, nothing is breaking besides the stock market and early signs that home prices are starting to fall.” (Source: fidelity.com 9/29/22)

There are always multiple factors that need to be watched that can directly affect equity markets. Here are four concerns that could be major factors in determining the direction of equity markets at this time:

The continuation of rising inflation rates.

The inflation rate is still not losing steam despite the Fed’s efforts. All eyes are on the Fed’s movements to

combat inflation, which has been and will continue to be a major factor in the economic environment at

this time.

Further interest rate increases.

The Fed’s key solution for fighting inflation is to raise interest rates. To date, their efforts have not produced satisfactory results. Interest rate increases this year have been consistently followed-up by a decline in equity markets.

Geopolitical unrest.

Equity markets do not like uncertainty and with the ongoing war between Russia and the Ukraine and concerns over a major conflict with China and Taiwan, geopolitical unrest continue to be something we are keeping a watchful eye on.

Recession Concerns.

There is a lot of talk about a recession. Fears that the Fed’s aggressive moves will plunge the economy into a deep recession have been a continual news headline. A recession is technically defined as having two successive quarters of economic decline. Empirically, we are in recession territory. However, with employment numbers still in good shape, decent economic earnings, and the housing market still healthy, the economy still has some areas of strength.

Fed Chairman Powell addressed recession fears during a press conference following the September Fed meeting. He shared that, “No one knows whether this process will lead to a recession or, if so, how significant that recession would be.”

Regardless of whether we indeed will experience a severe recession, investors should understand that volatility is likely to be here for a while.

As your financial professional, we are committed to keeping you apprised of any changes and activity that could directly affect you and your situation. Now is a key time to practice patience and resilience and to remain focused on your personal, long-term goals.

Inflation & Interest Rates

This year, we have experienced the fastest rise of inflation since the 1980s. Despite the Federal Reserve’s efforts to slow down this runaway train, inflation is still strong.

At the September FOMC meeting, Fed Chair Jerome Powell expressed that, “Our expectation has been we would begin to see inflation come down, largely because of supply side healing. We haven’t. We have seen some supply side healing, but inflation has not really come down.”

In their continued efforts to combat public enemy #1, the Fed increased their interest rates again by 7 basis points (or 0.75%) for a target range of 3.0% to 3.25%. This marked the third time the Feds have raised rates by 75 basis points and the fifth time they have increased rates in 2022.

Equity markets responded negatively to this news. The DJIA closed the day down 522.45 points (or

1.7%). The S&P 500 dropped 1.71% and after the close on that short announcement day in September,

was down more than 10% for the past month and 21% from its 52-week high. (Source: cnbc.com; 9/20/22)

With August’s year over year inflation rate being 8.3%, policymakers still have a long battle ahead when trying to bring inflation to a more stable pace. In November, the Federal Reserve will meet once again. It is anticipated that at that meeting, rates will again be increased.

At a post September meeting news conference, Powell stated he remains on course with his intentions expressed at the Fed’s annual symposium in August, “My main message has not changed since Jackson Hole. The FOMC is strongly resolved to bring inflation down to 2%, and we will keep at it until the job is done.” (Source: cnbc.com; 9/21/22)

Inflation is a real concern for Americans because it eats into our purchasing power and lifestyle. Anyone

who drives, eats, turns on the lights, swipes a credit card, or has living accommodations, is experiencing the effects of inflation. The four major area most Americans are feeling the pressure is at the grocery store, the gas pump, their electricity bill – and in housing costs, whether you are renting or buying.

It is always a good idea for investors to try to at least keep pace or exceed inflation rates. Median federal

funds rate projections from the recent FOMC meeting were revised for 2022, increasing to 4.4%,

1% higher than the previously projection in June of 3.4%. For 2023, projections increased from 3.8% to

4.6%, and for 2024 to 3.9% from 3.4%.

What does this mean for you? It’s very possible that interest rates above the last few years historically low rates will be here for some years to come. Since the 2010’s, American had been enjoying these historically low interest rates. Now, interest rates are front and center as the Fed stands by its commitment to combat inflation.

We continue to suggest that, if you haven’t already done so, to take a look at these areas of your financial situation:

- proactively pay off all non-essential interest-bearing debt.

- maintain liquidity for short-term purchases.

- if you have a mortgage, lock in your rate.

- If you have bonds in your portfolio, understand the duration of them; and

- review all income-producing investments.

As your financial professional, we are committed to keeping a vigilant eye on all aspects of financial planning that may affect you. Interest rates will continue to be near the top of our watchlist. If you are concerned about how interest rate increases may affect your portfolio, please connect with us to discuss any possible strategies that may help combat the effect on your personal situation.

The Bond Market and Treasury Yields

Treasury yields are thriving in this environment. Our chart shows the significant increase in yields we have experienced since the beginning of 2022 across the 5, 10, 20, and 30-year time ranges. As of September 30, 5-year notes yielded 4.06%, 10-year notes yielded 3.83%, 20-year notes yielded 4.08%, and 30- year notes reached 3.79%. The benchmark 10-year Treasury note had not seen these rates for over 12 years, when it reached a high of 3.93%.

Bond investing can be tricky and the opportunity to take advantage of favorable bond yields could be brief. Also, please remember, while diversification in your portfolio can help you reach your goals, it does not ensure a profit or guarantee against loss.

The 2-year treasury reached 4.30% on September 27, which is the highest it has been since August 2007. This milestone brings concern to many analysts as they watch the inverted yield curve get steeper – what many believe to be a strong indicator of economic downturn.

Bonds which have historically been held by investors as a balance to equities have had a very rough ride in 2022. When rates go up existing bond prices go down. Longer term bonds tend to be the ones most affected, so investors need to watch the duration or length of the bonds they hold.

If you’d like to explore how bonds could fit into your retirement income strategy, please contact us. We are monitoring how the Fed’s movements and rising interest rates are affecting bond yields.

Investor’s Outlook

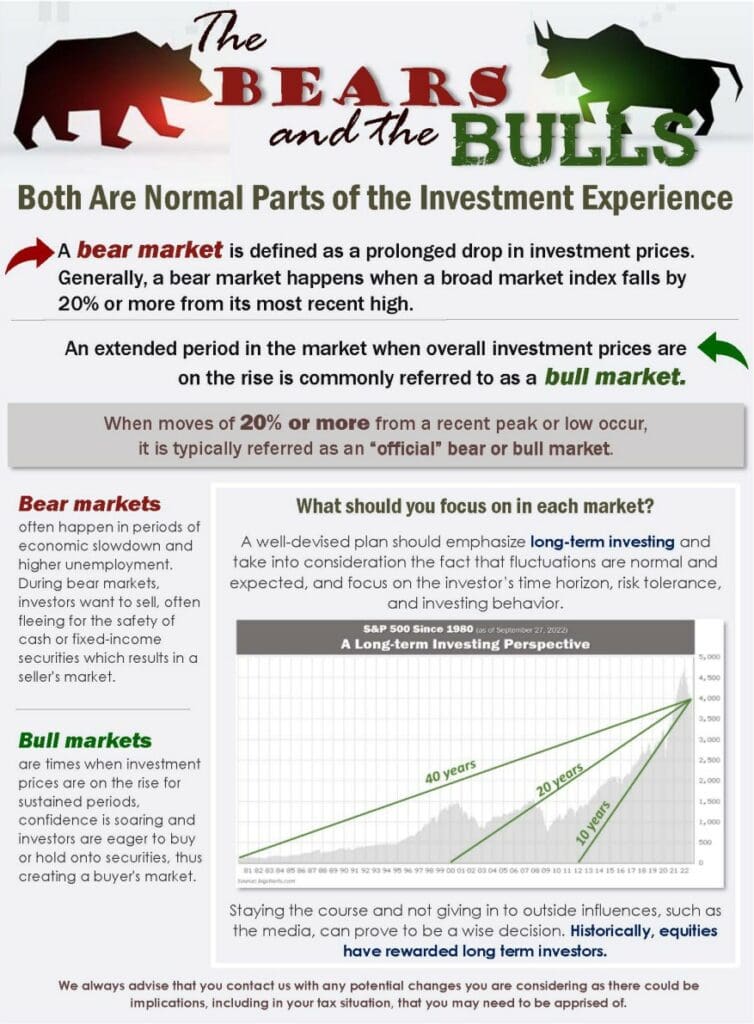

Can anyone predict the next 5, 10, or 50 years for investors? The answer is clearly, no. But, while past market results do not forecast future performance, it is helpful to look at history. During the 50 years

from 1970-2019, there were seven recessions, 10 bear markets and four distinct market crashes with losses in excess of 30% for the U.S. stock market. If you go back even further to the previous 50 years from 1920 to 1969, there were 11 recessions, 15 bear markets, and eight distinct market crashes with

losses in excess of 30% for the U.S. stock market. In other words, bear markets are a very normal and

reoccurring part of the investment experience. Since 1930, the market has been bearish for about 20.6 years. Conversely, this means that stocks have been favorable the other 72 years!

Many investors are speculating on how long this bear market will continue. While no one can decisively

predict when it will end, the good news is that it should, eventually end. The average bear market since the modern S&P 500’s inception in the 1920s lasted an average of 19 months. (Source: cnb.com; 6/13/22)

Those investors who chose to ride out even some of the longest bear markets were rewarded with significant returns. For example, from March 1937 to April 1942, the U.S. experienced an almost 62- month bear market. However, the bull market gain after this bear market was 325%. (Source: S&P Dow Jones Indices)

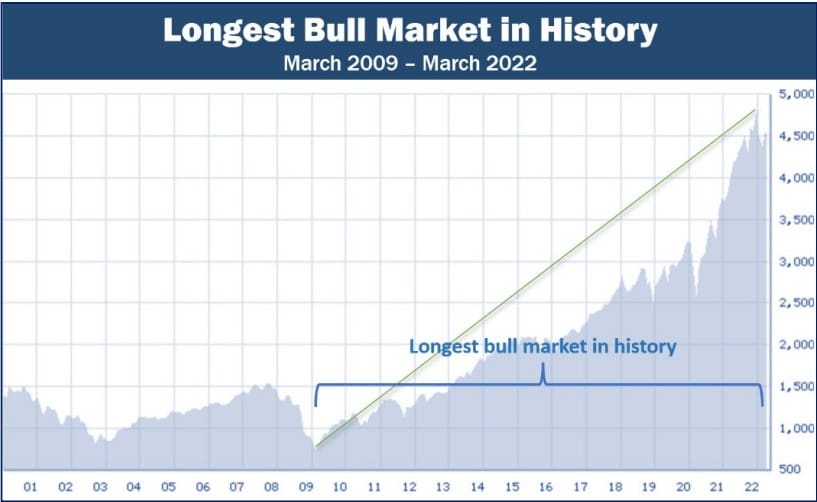

More recently, from March 2009 to March 2020, we experienced the longest bull market in history.

According to calculations on the website www.officialdata.org, if you invested $10,000 right before the bull market began in 2009, by 2020, that $10,000 would be about $55,817, or a hefty 458% return on investment or 15.41% per year. As billionaire investor and businessman Charlie Munger stated, “It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait.”

Until there are signs of slowing growth, the Fed will continue to charge forward on their fight against

inflation. With that, and the markets response to the Fed’s bold moves, recession woes will continue to be front and center. Wise investors have well-devised plans that take into consideration potential volatility so that there are no surprises when market fluctuations inevitably happen. While no one knows what each year brings, here are some strategies that investors should consider:

- Focus on your time in the market, not trying to time the market. Historically, equity investors

who focus on long-term goals and remained faithful to their personal, well-crafted plan have been rewarded. While it can be tempting to sell investments to avoid losses during a bear market, investors who find themselves still out of the market during a recovery can miss out on significant gains. Remember, investing in equities should be viewed as a long-term commitment! As your financial professional, our strategy is to devise a plan that includes how you will react to the ups and downs, including your time horizon, tax implications, liquidity needs, risk tolerance, and your overall personal objectives. - The cost of borrowing is continuing to rise. A good rule during rising interest rates is to maintain liquidity for any larger purchase you know or think you will have in the near future.

- Keep a level head and clear perspective. It’s easy to experience anxiety over today’s current environment, particularly if you listen to the news and read the headlines daily. Making rash moves or panicking are never good strategies. While it is prudent to stay apprised of what is happening around you, it is often a good practice to turn off the repetition of news that can cloud your judgement. As your financial professional, we are keeping a close eye on anything we feel may affect your situation. As always, if you have any concerns or questions, please contact our office.

- The current cycle we are experiencing may take some time. That is why we recommend proceeding with caution. Please call our office to discuss any concerns or ideas you have or bring them up at your next scheduled meeting. Prior to making any financial decisions, we highly recommend connecting with us so we can help determine your best strategy. There are often other factors to consider, including tax ramifications, increased risk, and time horizon changes when altering anything in your financial plan.

These are challenging times for investors, and we want you to be comfortable knowing that we are staying apprised of any situations that may affect your situation. Having a proactive approach to your

financial goals and a solid investment strategy is part of the overall client experience we provide.

As always, please feel free to connect with us with any concerns or questions you may have.

We pride ourselves in offering:

- Individualized advice tailored to your specific needs and goals.

- Consistent and meaningful communication throughout the year.

- A schedule of regular client meetings.

- Continuing education for all our team members on issues that may affect you.

- Proactive planning to navigate the changing environment.

Remember, a skilled financial professional can help make your financial journey easier. Our goal is to

understand your needs and create an optimal plan to address them.

While we cannot control financial markets, inflation, or interest rates, we keep a watchful eye on them. We can discuss your specific situation at your next review meeting, or you can call to schedule an appointment. As always, we appreciate the opportunity to assist you and your financial matters.

team@stablerwm.com | (425) 646-6327

Note: The views stated in this letter are not necessarily the opinion of LPL Financial and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice.

Securities and advisory services offered through LPL Financial, Member FINRA/SIPC and an SEC Registered Investment Advisor. Stabler Wealth Management and LPL are separate and unaffiliated. Stabler Wealth Management is not a registered investment advisor or broker-dealer. This article is for informational purposes only. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice as individual situations will vary. For specific advice about your situation, please consult with a lawyer, tax or financial professional. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation.

This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. The S&P 500 is an unmanaged index of 500 widely held stocks that is general considered representative of the U.S. Stock market. The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. There is no guarantee that a diversified portfolio will enhance overall returns out outperform a non-diversified portfolio. Diversification does not protect against market risk.

Sources: www.cnb.com; www.cnn.com; www.fidelity.com; www.barrons.com; www.officialdata.com; www.bigcharts.com. Contents provided by the Academy of Preferred Financial Advisors, 2022©

Category

Stay Informed

Join our mailing list to receive monthly newsletters with information that impacts your financial decisions.

Certified Financial Planner

In Business 35+ Years