3rd Quarter 2023 Economic Update

Historically, the third quarter is the worst quarter of the year in equity markets. 2023’s third quarter followed that trend. September was very uncomfortable for investors as volatility increased during this last month of the quarter. Equities moved lower in late September as the Federal Reserve refrained from raising rates, but announced there is a possibility of another rate hike this year. The prospect of interest rates staying higher for longer did not resonate well with investors.

Equities also took another downward ride in September, as the government waited until the 11th hour to pass a stopgap funding bill, narrowly avoiding a government shutdown.

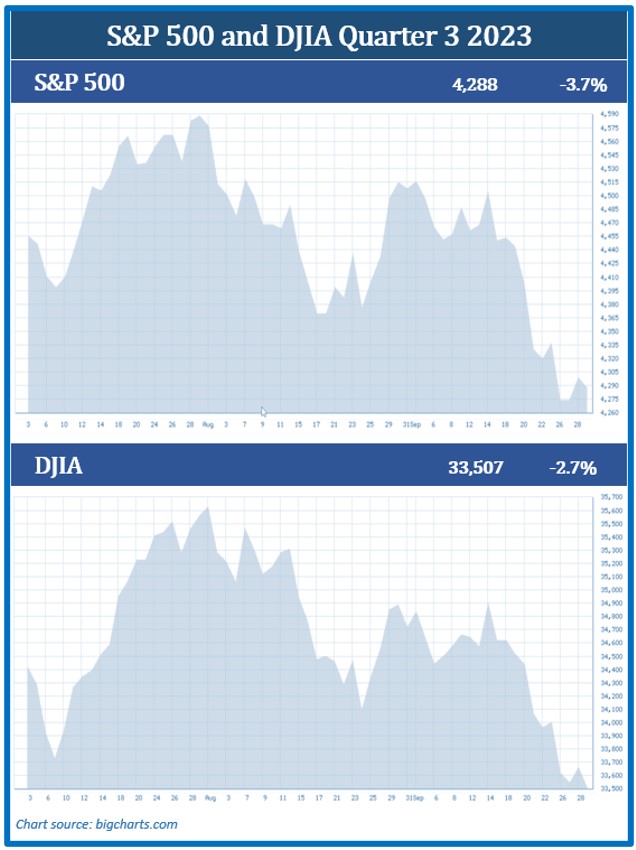

The major indexes ended the third quarter lower than they started. In September, the S&P 500 dropped 4.9%, and the Dow Jones Industrial Average (DJIA) fell 3.5% for the month. For the quarter, the S&P 500 fell 3.7%, ending its three-quarter-long gains streak. This major index closed the quarter at 4,288. The Dow Jones Industrial Average (DJIA) ended the quarter down 2.7%, closing at 33,507. (Source: Forbes.com; 10/5/23)

By the end of the quarter, some of the more optimistic outlooks from investors dwindled as concerns and volatility increased. Government and economic uncertainty, stubborn inflation, and the news of another potential rate hike this year took the lead on investor worries.

The quarter included the Fed once again increasing interest rates in July, a slight uptick in inflation, and continued talk of a pending recession; however, the US economy held its ground with a strong job market and consumer spending confidence.

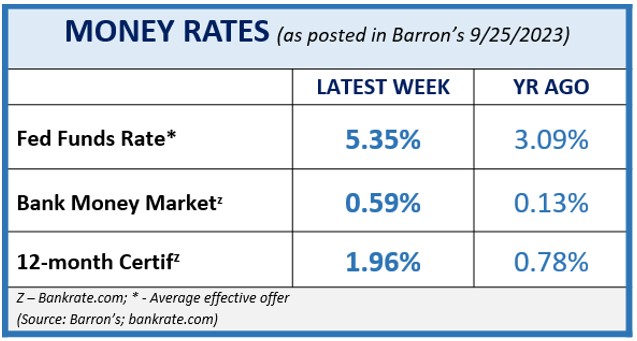

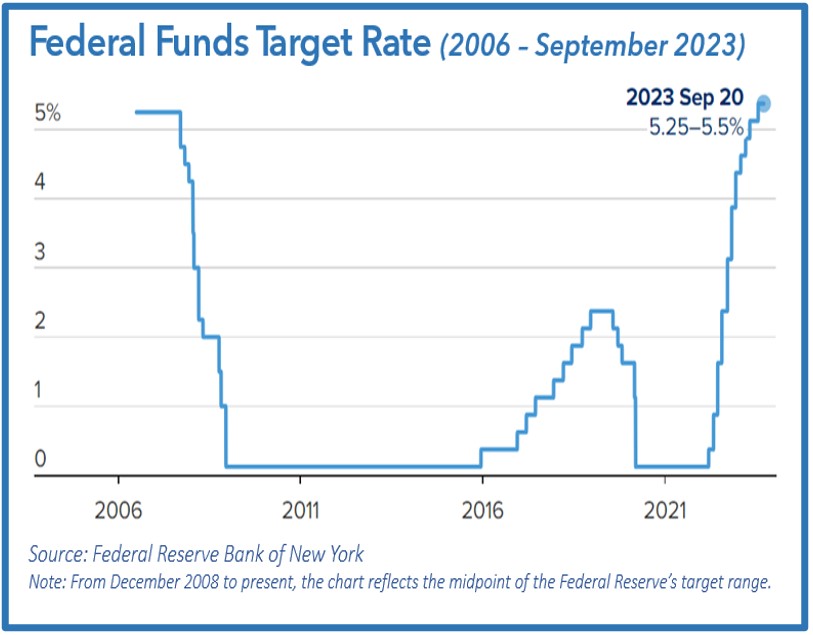

Personal consumption expenditure (PCE), which the Feds closely watch, increased 3.9% for the 12-month period ending August. At their September meeting, the Fed decided to keep the federal funds rate range at 5.25 – 5.50% and upgraded their view of the pace of the economy as “solid” rather than the “moderate” pace it had previously assigned.

They noted in their September statement that, “Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have slowed in recent months but remain strong, and the unemployment rate has remained low. Inflation still remains elevated.” (Source: federalreserve.gov; 9/20/23)

The labor market remained strong in the third quarter. Although inflation is continuing at a slow downward trend toward pre-pandemic levels, labor costs are increasing and this is placing a strain on businesses looking for employees. The current demand for labor keeps pushing wage inflation, with real wages being higher than before the pandemic. Unemployment has now been under 4% for 19 months in a row. This is a key economic indicator that the Fed watches closely.

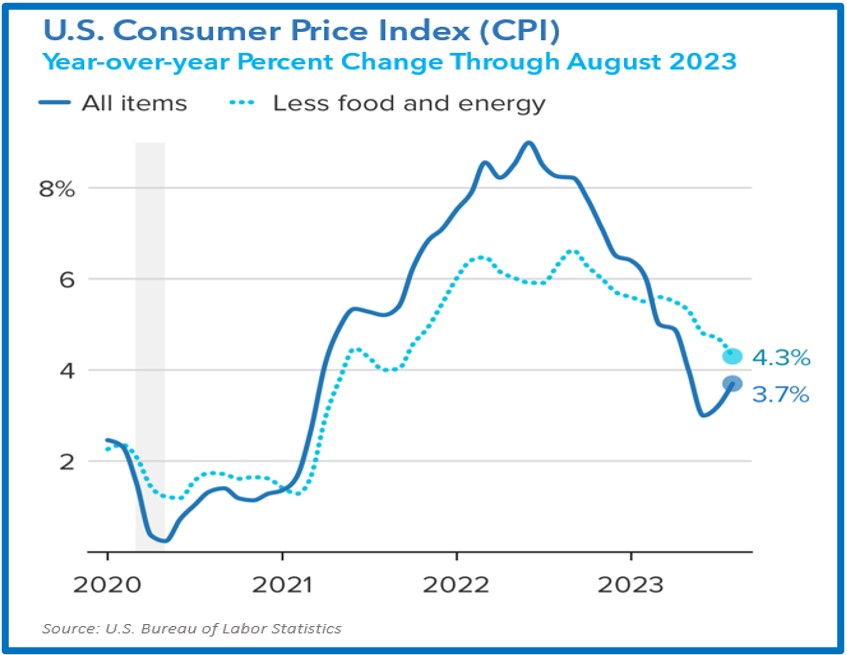

One setback during the quarter was in September when inflation numbers for August posted their biggest monthly increase for 2023. However, upon close examination, the core consumer price index (CPI) decelerated. Equities initially fell in response to the release of this data but rebounded shortly thereafter. September inflation is set to be released in late October; however, August’s inflation rate grew 3.7% year-over-year, a much better number than last August’s year-to-year inflation rate of 8.3%.

In late September, the House of Representatives cancelled their pre-planned two-week recess to avoid a possible government shutdown. A short-term funding bill was needed to be approved by Congress and President Biden by October 1, and as of late September, they had not yet passed a bill. Without it, a government shutdown was imminent. With just hours to spare, the House struck a deal, passing a 45-day stopgap government funding bill, diverting a potentially catastrophic event.

What does all this activity mean? Will the third quarter’s gloominess set us up for a stock-market rally in the coming months, or will uncertainty prevail and send U.S. equities further down the receding trend?

Historically, the fourth quarter of the year is the best quarter for the U.S. stock market, with an average gain of more than 4% since 1950.However, if we have learned anything from the past few years, anything is possible. As an investor, the third quarter confirms that volatility is still prevalent. This is not a time to become complacent. We remain firm in our philosophy that investing is a long-term commitment. Having a long-term-centered, diversified plan can help you weather market volatility and economic uncertainty. We know that short-term trading and investing can prove to be riskier and less tolerant of market fluctuations and instability and is not for everyone.(Source: fool.com; 10/2/2023)

As your financial professionals, we are committed to keeping you apprised of any changes and activity that could directly affect your unique situation. We are available to review your investments and make sure they are still congruent with your time horizon, risk tolerance, and goals.

This is a time to concentrate on your personal financial plan. Having a long-term-focused plan that is well diversified can help position you to manage volatility in the markets. We are available to review our clients’ investments and make sure they are still congruent with your time horizon, risk tolerance, and goals.

Inflation & Interest Rates

The Federal Reserve decided not to increase interest rates at their September session and the rate range remained at 5.25 – 5.50%. However, they signaled that another rate hike is likely to happen later this year due to the continued strength of the economy and the slight rise in inflation. “We are committed to achieving and sustaining a stance of monetary policy that is sufficiently restrictive to bring inflation down to our 2 percent goal over time,” stated Fed Chair Jerome Powell in the Press Conference following the FOMC meeting in September.

“We will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data,” Powell said in a keynote address. “It is the Fed’s job to bring inflation down to our 2% goal, and we will do so.” (Source: reuters.com; 8/25/2023)

In September, Consumer Price Index (CPI) reports for August were released. The White House released their August 2023 Consumer Price Index notice, announcing that inflation was 0.6% in August and 3.7% over the past 12 months. Both rates were a step up from recent inflation reports. This was the biggest monthly increase to date for 2023. The main culprit for this jump was the significant price increase of gasoline, which flew over 10.6% in August. Consumers cringed at the price of filling up their gas tanks and the cost of fuel and food continued to put a strain on budgets. Transportation costs, including gas, are the second largest expenses for U.S. households, the first being housing costs.

Many economists believe this slight uptick will be short lived. “This should just be a temporary interruption of the downward trend,” said Andrew Hunter, Deputy Chief U.S. Economist at Capital Economics. He continued, “Broadly, we’re already seeing pretty clear signs the situation is approaching normal again.” (Source: www.cnbc.com, 9/13/23)

To put things in perspective, without the energy and food sectors, the core inflation only rose 0.1% percentage point during this period. When you look beneath the numbers, the year-over-year percentage change for the CPI through August 2023 actually went down in August, if you remove food and energy.

The consumer price index measures the average change in price across a broad array of goods and services. The good news is that even in August, the core CPI continued to decelerate. The core CPI is a better indicator of where inflation is headed, and the Fed focuses more on this data to help them determine their approach to battling inflation.

Like all aspects of financial planning that may affect you, we are keeping a vigilant eye on interest rates and inflation. If you’d like to know how these may affect your portfolio, please contact us to discuss any strategies that may help combat the effect on your personal situation. While we cannot predict what the Fed’s next move will be, we are keeping a watching eye on key economic indicators, such as the CPI.

The Bond Market and Treasury Yields

While equities moved down, bond yields moved up. After the Federal Reserve meeting in September, bonds yields rose, continuing their multi-decade highs. On Wednesday, September 20, the yield on the benchmark 10-year treasury note closed at 4.35%.

On September 27, the 10-year note hit a high of 4.61%, its highest rate since 2007. To end the third quarter, the 10-year treasury note closed at 4.59%, the 20-year treasury ended at 4.92% and the 30-year note closed at 4.73%. (Source: treasury.gov)

Since April of 2022, we have seen an inverted yield curve, meaning longer maturities have a lower yield than some short maturities. This trend remained in the third quarter, with one-year treasury yields ending the quarter on September 29 at 5.55%, and the 10-year, 20-year, and 30-year treasury yields ending at 4.59%, 4.92%, and 4.73%, respectively. Historically, this has been a key indicator that we should carefully watch for a pending recession. However, the U.S. economy is still strong, due to a continued low unemployment rate, wage growth, and slowing inflation. As financial professionals, these are all economic indicators that we need to watch and monitor.

For anyone who is interested in exploring adding more bonds as part of a diversified portfolio, please contact us. As your wealth manager, we want to help you make the best decision for your portfolio. Please remember, while diversification in your portfolio can help you pursue your goals, it does not ensure a profit or guarantee against loss.

Please keep in mind that if the Fed decides to ease up or reverse interest rates, that will narrow the opportunity to get lower-risk, higher yielding bonds quickly. For right now, the Fed has signaled potentially one more interest rate increase this year, keeping the window open for higher short-term rates. We will continue to monitor how the Fed’s movements and how rising interest rates are affecting bond yields.

Investor’s Outlook

Investors need to enter the fourth quarter with an understanding that it might be a volatile one. The sentiment that interest rates would be lowered in the near future dwindled during the third quarter with the news of a possible rate hike before the end of the year. Most analysts believe the interest rate hiking cycle is peaking, however, “higher for longer” has become the new interest rate theme.

Historically, the fourth quarter is a strong quarter for U.S. stock markets. Since 1928, including some very tough Octobers, like October 1987, during the fourth quarter, the S&P 500 on average has had positive returns. (Source: fool.com; 10/2/2023).

This year, there are some key concerns that could affect the trajectory of the markets in the near future. Oil prices have recently soared and this could continue. Also, there is monetary policy uncertainty, and the race for the White House may prove to be one of the most caustic and challenging elections ever.

The Federal Reserve will also be keeping a close eye on key indicators such as housing, labor markets, and core goods. It is critical that the Fed does not overshoot its target and trigger the U.S. economy into a speedy downturn. Most of us are hoping for a “soft enough landing” and averting a recession, a primary objective of the Feds.

Keep in mind that a soft landing could mean slow economic growth for some time. Regardless of the outcome, it is always prudent to watch your expenses and make smart money and investment decisions. Having some financial liquidity, staying out of debt, and planning for any large cash commitments, such as a wedding or new car purchase, should be taken into consideration in your financial plan.

We believe in proactive preparation to ensure you have your personal financial situation set up to best weather anything the economy may bring. The past few years have taught investors that it’s healthier to expect the unexpected.

From an investor standpoint, we stand by our belief that investing in equities is a long-term commitment. We believe that volatility is still prevalent and you should be prepared to proceed with caution. The coming months ahead could bring market challenges and long-term stability needs to be a key goal for smart investors.

Please remember, historically, investors with a long-term plan that stayed the course and remained diversified and invested were rewarded. We believe this still holds true for today’s investors. Savvy investors have a long-term mindset and well-devised and diversified financial plans.

We are not in the business of trying to predict the future. We want to provide you with a solid financial strategy that is designed to best weather any market environment. While past performance is not a guarantee of current or future results, history shows us that returns from equities after a recession have been fruitful.

Heading into the fourth quarter, we will continue to keep an eye on inflations rates, economic growth data, and monetary policy moves. There is a strong possibility that the Fed will increase rates (possibly by .25%) before the end of the year. Obviously, this will depend on the data the Fed receives.

The end of the year is a good time to go over certain key items that can help keep your finances in good order. Some year-end items to consider include:

- Maxing out your retirement contributions (for those of you still working). If you haven’t already, maximize your retirement savings contributions into your 401(k) or any employee-sponsored plan. If you don’t have a workplace plan, call us to see if you can contribute to an IRA.

- Reviewing if partially or fully converting to a Roth IRA makes sense and what that looks like taxwise. Warning: This is complicated, so please contact us to see whether this is a good option for your situation.

- Proactively reviewing your plan for future college expenses by starting or contributing to a 529 college savings plan.

- Reviewing any year-end tax harvesting opportunities. (i.e., looking into selling stocks and funds that have lost value to offset your taxes).

- Revisiting your annual budget for 2024. Is your budget consistent with your needs and goals?

- Rechecking your estate plan (including your beneficiaries).

- Finalizing your year-end charitable giving (including donating to your favorite charities and benefit from knowing you are helping others).

The coming months could be filled with uncertainty and some heavy market volatility. A few tips to help you through uncertain times are:

- Keep your head down and minimize your viewing or responding to any mass media, including the news and social media.

- Live within your means and avoid incurring any more debt than necessary.

- If possible, continue to add to your savings.

- If you need to, review your financial situation directly with us.

We take pride on offering our clients quality service that includes:

- A proactive, individually tailored approach to each client’s financial goals and needs.

- Consistent and meaningful communication throughout the year.

- A schedule of regular client meetings.

- Continuing education for all our team

members on issues that may affect our clients. - Proactive planning to navigate the changing environment.

We always recommend discussing any changes, concerns, or ideas that you may have with us prior to making any financial decisions so we can help you determine your best strategy. There are often other factors to consider, including tax ramifications, increased risk, and time horizon changes when altering anything in your financial plan.

Please remember that as a valued client, we are accessible to you! Feel free to contact us with any concerns or questions you may have.

We appreciate the trust and confidence you place in our firm.

team@stablerwm.com | (425) 646-6327

Securities and Advisory services are offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC.

Note: The views stated in this letter are not necessarily the opinion of LPL Financial, and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Investors should be aware that there are risks inherent in all investments, such as fluctuations in investment principal. With any investment vehicle, past performance is not a guarantee of future results. Material discussed herewith is meant for general illustration and/or informational purposes only, please note that individual situations can vary. Therefore, the information should be relied upon when coordinated with individual professional advice.

This material contains forward looking statements and projections. There are no guarantees that these results will be achieved. All indices referenced are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

The S&P 500 is an unmanaged index of 500 widely held stocks that is general considered representative of the U.S. Stock market. The modern design of the S&P 500 stock index was first launched in 1957. Performance prior to 1957 incorporates the performance of the predecessor index, the S&P 90. Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal. Past performance is no guarantee of future results. CDs are FDIC Insured and offer a fixed rate of return if held to maturity. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed.

There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. There is no guarantee that a diversified portfolio will enhance overall returns out outperform a non-diversified portfolio. Diversification does not protect against market risk.

Sources: www.whitehouse.gov; www.reuters.com; www.fool.com; www.barrons.com; www.cnbc.com; www.msn.com; U.S. Department of Treasury; Contents provided by the Academy of Preferred Financial Advisors, 2023©

Category

Stay Informed

Join our mailing list to receive monthly newsletters with information that impacts your financial decisions.

Certified Financial Planner

In Business 35+ Years