How Much Microsoft Stock Is Too Much—and What to Do About It

After a remarkable run over the past decade, Microsoft stock has faced renewed volatility in early 2025 amid broader market turbulence. While the recent decline has led many to take a “let it ride” approach, it also serves as a timely reminder to assess your Microsoft stock concentration—and whether it aligns with your financial goals.

Even with the recent pullback, Microsoft has still doubled over the last five years and climbed nearly 9x over the past decade. For many Microsoft professionals, this growth has resulted in a sizable (and sometimes risky) portion of their net worth being tied to a single company. So how much Microsoft stock is too much? And if you’re overexposed, what should you do next?

Let’s dive in!

The Real Question: What’s the Right Amount for You?

Everyone’s personal situation is different, and the right level of exposure varies depending on your broader financial picture, your proximity to retirement, and your risk tolerance. There are two ways to assess the right amount of Microsoft stock for you:

Monte Carlo Stress Testing

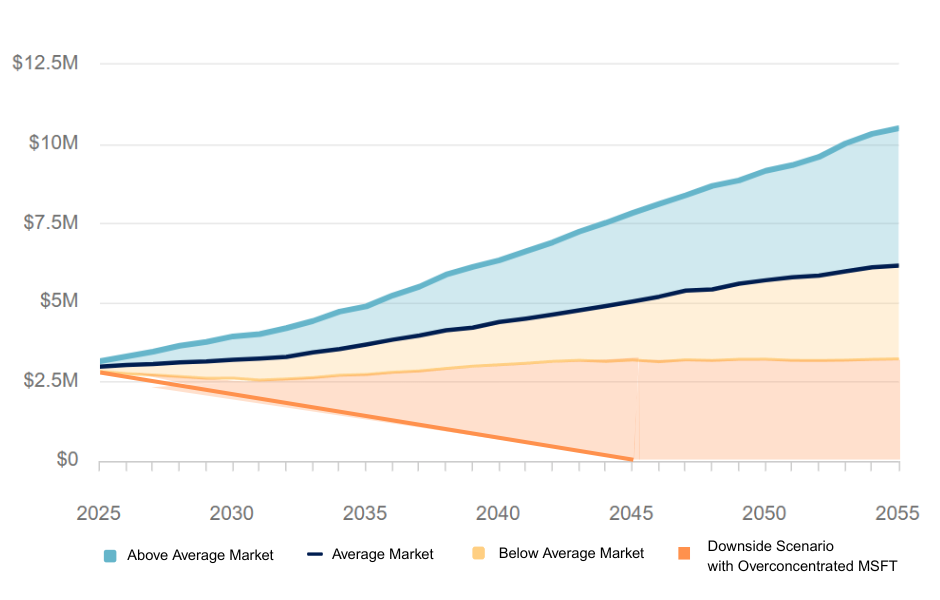

For those later in their careers or within arm’s reach of retirement, we recommend running a Monte Carlo stress test to determine how a prolonged Microsoft downturn could affect your long-term financial security. In this simulation, we analyze what happens if Microsoft underperforms for an extended period—could your financial plan still succeed, or could it force a delay in your retirement—or even require returning to work? This exercise can be incredibly eye-opening and provide the clarity needed to take action with confidence.

The Quick and Dirty: The 10% Rule of Thumb

If you’re looking for a simple starting point, consider this: having more than 10% of your total investment portfolio in one individual stock puts you in the concentration danger zone. For Microsoft employees, this risk is amplified because your paycheck, RSUs, and potentially even your spouse’s income may all depend on the same company.

“Yes, That’s Me. What Should I Do Now?”

First, you’re not alone. The majority of Microsoft professionals we meet with are in the same boat—with many holding well over $1 million in Microsoft stock. The good news? There are several proactive steps you can take:

1. Start with the Low-Hanging Fruit

As discussed in our recent article on Microsoft stock volatility, there are tax-efficient moves you can make right away:

- Sell vested RSUs as they vest. This is often a tax-neutral transaction and allows you to treat the RSUs like a cash bonus.

- Reallocate within your 401(k) where possible to reduce Microsoft exposure without triggering a taxable event.

- Target lots at a loss in your brokerage account to sell without incurring capital gains.

2. Evaluate What You Can Sell at Favorable Tax Rates

Even if you’re in a high-income tax bracket, keep in mind that long-term capital gains are taxed more favorably than ordinary income. You only pay tax on the gain, and many clients are surprised by how much they can sell without pushing into a higher tax bracket.

We suggest reviewing your specific tax lots to identify the most strategic shares to sell—minimizing your tax impact while improving your overall portfolio diversification.

This liquidity can be especially useful in early retirement when you’re bridging the gap to Medicare or managing premium costs on ACA health insurance plans.

3. Don’t Fear “Selling Low”

Even if Microsoft stock has pulled back, remember—if you’re reinvesting the proceeds into a diversified portfolio, you’re not exiting the market. And with many stocks also down, you’re often selling low and buying low.

For those within a few years of retirement, this is also an opportunity to review your overall asset allocation. Many Microsoft professionals in this phase are overweight equities, and this is a critical time to bring your portfolio in line with your income needs and risk tolerance.

4. Consider Hedging Strategies for Excess Exposure

For those that remain in the over-concentration danger zone even after the above steps, one advanced strategy we often evaluate is a “collar hedge.” This options-based strategy acts like insurance—providing downside protection without triggering a taxable event from selling your stock.

This can serve as a bridge solution while you gradually diversify your Microsoft stock over several years in a more tax-efficient manner.

The Bottom Line: Letting It Ride Is a Decision

Staying the course with your Microsoft stock exposure might work out—but it’s a choice with real consequences. In most scenarios, we find that being more proactive can help build a more resilient portfolio and increase your odds of reaching your long-term financial goals. You’ve already won by accumulating so much in Microsoft stock. Now it’s time to protect that win.

Our team of Certified Financial Planners specializes in helping Microsoft professionals navigate these complex decisions. If you’re unsure of the right strategy for your situation, schedule a complimentary consultation and let’s chart the best course for your future.

Overconcentration Increases the Risk of Running Out of Money in Retirement

Contact Us:

team@stablerwm.com | (425) 646-6327

No strategy assures success or protects against loss. Stabler Wealth Management and LPL Financial are not affiliated or endorsed by Microsoft.

Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss.

Asset allocation does not ensure a profit or protect against a loss.

Securities and Advisory services are offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC. Stabler Wealth Management is not registered as a broker-dealer or investment advisor.

Category

Stay Informed

Join our mailing list to receive monthly newsletters with information that impacts your financial decisions.

Certified Financial Planner

In Business 35+ Years